Business & Economy

CBN Stops Free Withdrawals For Customers Using Other Banks’ ATMs

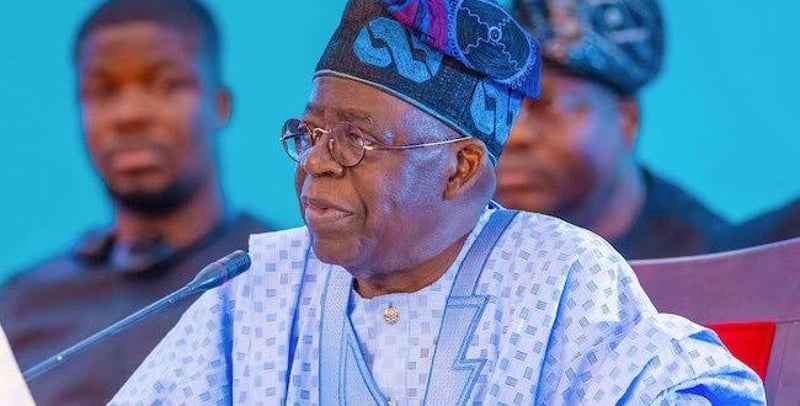

Business & Economy

Tinubu Welcomes Nigeria’s Removal from FATF Grey List, Pledges Continued Financial Reforms

Social Dairy3 days ago

Michael Opeyemi Bamidele Honoured as Oluomo of Iyin-Ekiti

Share***A Historic First in His 30-Year Public Career It was a colourful scene of culture, music, and prestige on Saturday...

Politics4 days ago

Bayelsa Governor Douye Diri Set to Join APC on Monday as Tinubu, Party Leaders Prepare Grand Welcome

ShareBayelsa State Governor, Douye Diri, is poised to officially defect to the All Progressives Congress (APC) on Monday, in what...

Defence and Security5 days ago

TINUBU TO SERVICE CHIEFS: NO MORE EXCUSES, DEFEAT TERRORISTS AND BANDITS NOW

SharePresident Bola Ahmed Tinubu has charged the newly appointed service chiefs to intensify military operations and ensure the total defeat...

Politics5 days ago

TINUBU HANDS OVER TARABA GOVERNOR AGBU KEFAS TO APC CHAIRMAN AHEAD OF DEFECTION

SharePresident Bola Ahmed Tinubu has formally handed over Governor Agbu Kefas of Taraba State to the National Chairman of the...

News5 days ago

Senate Confirms Bernard Doro as Minister of Humanitarian Affairs

ShareThe Senate has confirmed the nomination of Bernard Doro as Nigeria’s new Minister of Humanitarian Affairs and Poverty Alleviation. President...